Blog

Strong increases in cash rental rates in Iowa

This is the first post from Dr. Alejandro Plastina, Farm Foundation’s inaugural Agricultural Economics Fellow. He is one of several contributors we anticipate featuring as we re-launch our Farm Foundation blog in an effort to provide more frequent and useful information to stakeholders across food and agriculture.

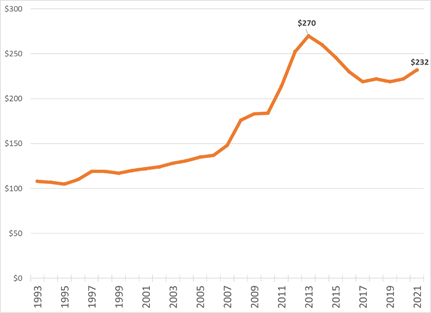

The most recent annual survey of cash rental rates for Iowa farmland shows that rates increased, on average, by 4.5 percent in 2021 to $232 per acre (Plastina and others, 2021). This is the first substantial increase in cash rents since 2013, when rents peaked and four years of declining rents and three years of relatively stable rents followed (figure 1). In comparison, nominal corn and soybean prices received by farmers in Iowa declined by 31 and 14 percent, respectively, since mid-2013.

Iowans supplied 1,363 usable responses about typical cash rental rates in their counties for land producing corn and soybeans, hay, oats and pasture. Of these, 41 percent came from farmers, 33 percent from landowners, 11 percent from professional farm managers and realtors, 9 percent from agricultural lenders, and 6 percent from other professions and respondents who chose not to report their status. Respondents indicated being familiar with a total of 1.5 million cash rented acres across the state.

There was considerable variability across counties in year-to-year changes, as is typical of survey data, but 76 out of the 99 Iowa counties experienced increases in average rents for corn and soybeans. The report also shows typical rents for alfalfa, grass hay, oats, pasture, corn stalk grazing, and hunting rights in each district.

Survey shows rent increases in all districts and across land qualities

The survey was carried out by Iowa State University Extension and Outreach. Statewide, reported rental rates for land planted to corn and soybeans were up from $222 per acre last year to $232 in 2021, or 4.5 percent. This percent increase is slightly less than two-thirds of the percent increase in Iowa farmland values between March 2020 and March 2021 reported in surveys conducted by the Iowa REALTORS Land Institute (2021) and summarized in AgDM File C2-75, Farmland Value Survey (REALTORS Land Institute).

However, the 14.1 percent accumulated decline in rental rates since 2013 is in line with the cumulative 13.3 percent decline in land values over the same period reported in the Iowa Land Value Survey published by the ISU Center for Agriculture and Rural Development (AgDM File C2-70, Farmland Value Survey).

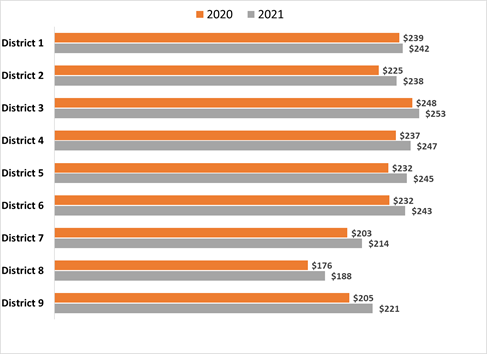

Different regions experienced different increases in cash rents: from 1.3 percent in Crop Reporting District (CRD) 1 to 7.8 percent drop in CRD 9 (figure 2). Except for Northwest and Northeast Iowa (CRDs 1 and 3), where average rents increased by less than $5 per acre, all CRDs experienced at least a $10 increase in average rents.

All land qualities have seen their average cash rents increase by similar percentages. High quality land experienced a 3.9 percent increase, from $257 per acre in 2020 to $267 in 2021.

Medium quality land experienced a 4.5 percent increase, from $223 per acre in 2020 to $233 in 2021.

Low quality land experienced a 4.8 percent increase, from $188 per acre in 2020 to $197 in 2021.

Cash rents up in other Midwestern states

According to a regional survey of bankers conducted by the Federal Reserve Bank of Chicago, cash rental rates for the Seventh Federal Reserve District climbed 4 percent from 2020 to 2021. For 2021, average annual cash rents for farmland were reported up by 2 percent in Illinois, 4 percent in Indiana, 5 percent in Iowa, and 5 percent in Wisconsin (Oppedahl, 2021). Preliminary survey results from Nebraska show increases in cash rents ranging from 2% to 12% across all agricultural statistics districts for dryland, gravity irrigated, and center pivot irrigated cropland, as well as on pastureland (Jensen and Stokes, 2021).

Setting rents for next year

Survey information can serve as a reference point for negotiating an appropriate rental rate for next year. However, rents for individual farms should be based on productivity, ease of farming, fertility, drainage, local price patterns, longevity of the lease and possible services performed by the tenant.

Three major factors with the potential to influence future cash rents are crop prices, government payments, and land values. Corn and soybean prices received in Iowa peaked in August 2012 at $7.90 and $16.80 per bushel, respectively. In March 2021, corn and soybean prices received by farmers in Iowa averaged $4.89 and $13.30 per bushel and, despite the run up in prices observed since July 2020, they accumulate a 38% and 21% decline since August 2012 (figure 3). The U.S. Department of agriculture is currently projecting average corn and soybean prices for the 2021/22 marketing year at $5.70 and $13.85 per bushel, respectively. These higher prices would improve net farm income with respect to last year, but would not be able to offset the reduction in income from lower government payments. In February 2021, the Economic Research Service forecast an 8.1 percent reduction in net farm income between 2020 and 2021.

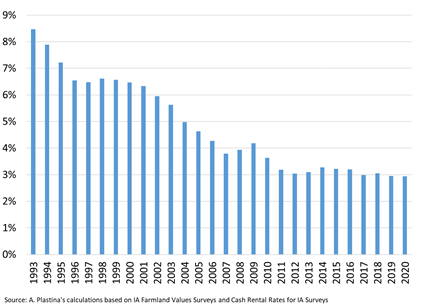

A major factor considered by landowners when negotiating cash rents is the return on their farmland investment. Figure 4 shows the evolution of the ratio of average cash rents to average land values in Iowa. It suggests that the average return on investment for landowners who cash rent their land to operators has followed a declining trend since the early 1990s, stabilizing at around 3% after 2010. Note that this ratio does not measure net returns because ownership costs, such as real estate taxes, are not taken into account in its calculation. However, it is indicative that landowners (whose goal is presumably to obtain a reasonable rate of return on their real estate assets) will likely be reticent to accept lower cash rents in the future unless land values continue to decline. However, with current interest rates at historically low levels and early indications of potentially increasing inflation risks, future interest rates are likely to be higher than current ones. As a result, the opportunity cost for landowners would increase and there might be pressure to ask for higher rents. Additionally, Iowa farmland values increased by 7.8% between September 2020 and March 2021 (Realtors Land Institute), putting more upward pressure on cash rents for 2022.

About the author

Dr. Alejandro Plastina is a 2021 Farm FoundationAgricultural Economics Fellow. He is an Associate Professor/Extension Economist in the Department of Economics at Iowa State University, specializing in agricultural production and technology, with an emphasis on farm business and financial management.

References

Jensen, J., and J. Stokes. 2021. “The Impact of COVID-19 and Economic Policies on Nebraska Farm Real Estate in 2021.” Cornhusker Economics, University of Nebraska-Lincoln. March 10. Available at https://agecon.unl.edu/cornhusker-economics/2021/The-Impact-of-COVID-19-and-Economic-Policies-on-Nebraska-Farm-Real-Estate-in-2021.pdf. Accessed on 5/29/2021.

Oppedahl, David. 2021. AgLetter, No. 1992. May. Federal Reserve Bank of Chicago. https://www.chicagofed.org/publications/agletter/2020-2024/may-2021.

Plastina, A., A. Johanns, A. Gleisner, and A. Qualman. Cash Rental Rates for Iowa 2021 Survey. Iowa State University Extension and Outreach, Ag Decision Maker File C2-10. Available at https://www.extension.iastate.edu/agdm/wholefarm/pdf/c2-10.pdf.